How Big Banks Turned Mortgages Into Cash Machines - And How The Risk May Be Passed Onto You

Canada’s big banks have become very good at turning mortgages into steady cash flow. They lend at attractive rates, use mortgage insurance to protect themselves, and pass the remaining risk to other players in the system. The result is a very profitable, and relatively safe, business for them. But the risks have not disappeared — they have just been redistributed.

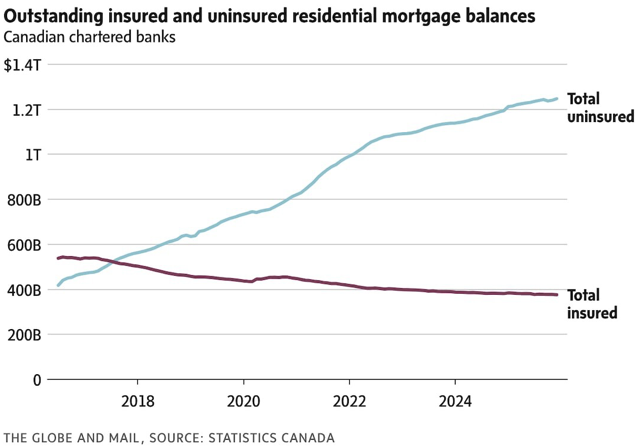

How mortgage risk is packaged up

Mortgage lenders in Canada fall into four main buckets: banks, credit unions, mortgage finance companies (MFCs), and mortgage investment entities (MIEs). Banks, credit unions, and most MFCs mostly lend to prime borrowers, where the risk is lower and the business is stable. MIEs, including MICs and private lenders, focus on subprime borrowers, where returns are higher and the risk is much more obvious.

That is why you will often see higher mortgage rates for private lending and MICs. The elevated returns reflect the fact that those products are not as safe as prime bank mortgages. Some MICs have struggled to keep up when delinquencies rise, and a few have had to limit redemptions or pause distributions to investors.

How insurance shifts risk away from banks

For many Canadians, the real story is the role of mortgage insurance. When you put less than 20% down, mortgage default insurance is mandatory. The three main insurers — CMHC, Sagen, and Canada Guaranty — essentially take on the risk that the bank might lose money if a borrower defaults and the home sale does not cover the outstanding loan.

Despite the scale of this business, the losses have been tiny. In 2024, CMHC took in $2.3 billion in premiums and fees but paid out only $45 million in claims across its massive portfolio. That is a loss rate of essentially nothing — 0.01%. Even if you narrow it down to single-family homes, the loss rate is still only 0.02%. That tells you that insured prime mortgages are much safer than people often think.

Where the risk really sits

The tricky part is that the risk is not gone; it has just moved. Taxpayers are indirectly on the hook through the federal guarantee that supports Sagen and Canada Guaranty, and banks are protected by the insurance system. The real risk is now sitting mostly in the subprime and private lending space, in MICs and MIEs, and in the pockets of investors who chase higher yields without fully understanding the risk.

That is why some MICs have had to curb redemptions or suspend payouts — their underlying loans are sometimes more vulnerable than the marketing material suggests.

A real-life example

Imagine two investors:

• Investor A buys a MIC that promises 8–9% returns backed by private mortgages on subprime borrowers. The returns look great, but the portfolio is loaded with riskier loans and higher delinquency potential.

• Investor B invests in a diversified, low-fee, broadly diversified real estate fund that does not rely on subprime lending. The returns are more modest, but the risk is much lower and the exposure is more spread out.

When housing stress increases, Investor A may see distributions cut or redemptions paused, while Investor B is more likely to weather the storm. The difference is not the market — it is the risk profile.

What this means for you

If you are a homeowner, the main takeaway is that the safest mortgage products are still the prime, insured mortgages from the big banks. They are protected by insurance, strong regulation, and relatively low loss rates. The riskier products are usually found in the subprime and private lending world, where the returns are higher but the risk is also higher.

If you are thinking about using a MIC, a private lender, or another high-yield mortgage product, it is important to understand the risk and to ask how much of the portfolio is exposed to subprime borrowers and how delinquencies are being managed.

How to be smart about it

• Focus on understanding the risk, not just the return.

• Ask how much of the portfolio is in subprime versus prime lending.

• Read the fine print on redemptions, distributions, and loss history.

• If you are unsure, speak with a mortgage professional or financial advisor before committing.

If you want help understanding how different mortgage products and risk levels fit into your overall financial plan, reach out to Mr. Mortgage today.

Kechanth Kannan | Mr. Mortgage

Phone: +1 (647) 554-2718

Instagram: @_mrmortgage