Why Nearly Half of Canadian Homebuyers Still Choose Mortgage Brokers in 2026

Image courtesy of The Globe and Mail

You might think digital apps and online banking would have made mortgage brokers obsolete by now.

Think again.

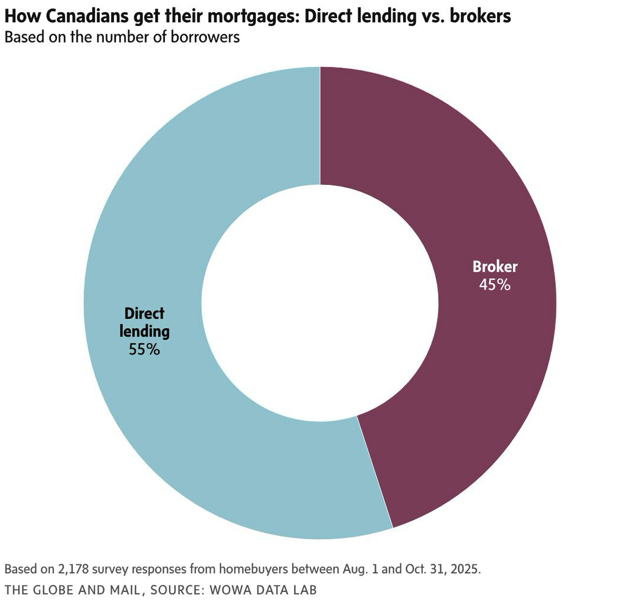

A recent WOWA Data Lab survey of over 2,100 recent homebuyers revealed that 45% still used a mortgage broker to secure their mortgage—proving human expertise remains essential in Canada’s complex lending landscape.

Despite fintech hype, here are the four rock-solid reasons brokers continue dominating the market:

1. Access to Unadvertised “Real” Rates

Banks love posting sky-high “advertised rates” for headlines, then quietly offering much better pricing to qualified borrowers through brokers. Scotiabank is the poster child—they barely advertise mortgage rates publicly but give brokers their most competitive pricing.

The math: That 0.25-0.50% difference brokers negotiate? On a $500K mortgage, that’s $15K-$30K in interest savings over 5 years.

Big 6 Bank Broker Participation:

✅ Most active: Scotiabank, TD, BMO

⚠️ Selective: National Bank, CIBC

❌ No brokers: RBC

2. Solutions for “Declined” Borrowers

Even perfect credit scores get declined by Big Banks. Why? Self-employment income quirks, short employment history, or just “doesn’t fit our box.”

Brokers unlock B-lenders, credit unions, and niche products that turn “no” into “yes.” No upfront fees for prime borrowers either—lenders pay us ~1% commission.

3. Closing the Knowledge Gap

Most Canadians don’t know:

Your bank expects rate negotiation (first offer = worst offer)

Loyalty = higher rates (banks save best pricing for new clients)

30-year mortgages don’t exist in Canada

Stress tests apply even to renewals

First-time buyers especially need this guidance. Brokers demystify the process so you make informed decisions, not emotional ones.

4. Digital Lending Still Sucks (Sorry, Fintech)

True end-to-end digital mortgages require:

Open banking (not here yet)

Real-time CRA income verification (not here yet)

Automated underwriting (getting closer, but not there)

Until then, online “pre-approvals” are mostly marketing. Real approvals still need human underwriting.

Sarah’s Story: The Broker Difference

Sarah (first-time buyer, $420K condo):

Bank branch: Offered 5.49% fixed

Online lender: 5.39% (after 2 days of back-and-forth)

Mortgage broker: Secured 4.89% through Scotiabank + $2,500 cashback

Monthly savings: $98. 5-year total: $5,880. Sarah didn’t pay me a dime.

Why Brokers Aren’t Going Anywhere

Canada’s mortgage system is deliberately complex—stress tests, LTV ratios, GDS/TDS calculations, regional pricing differences. Digital can’t replicate the relationship-driven negotiation that unlocks true market rates.

2026 prediction: As rates stabilize and renewals accelerate, broker usage will climb toward 50%+.

The Bottom Line

Brokers = free rate negotiators with access to 20+ lenders, complex solutions, and insider knowledge. No commissions, no risk, massive upside.

Considering buying, renewing, or refinancing? Skip the bank branch line and the fintech frustration. I’m Mr. Mortgage (Kechanth Kannan)—your direct line to Canada’s best unadvertised mortgage rates.

📸 Instagram: @_mrmortgage

45% of smart Canadian homebuyers can’t be wrong. Let’s get you better mortgage terms.